Small businesses serve as a central pillar to the U.S. economy and local communities. They comprise 99.9 percent of all businesses and employ nearly half of private-sector workers, contributing to the financial security of millions of households.

But small businesses face a growing threat: the increasing frequency and intensity of severe weather hazards such as hurricanes, wildfires, and heat waves. Forty percent never reopen after a natural disaster, and an additional 25 percent close a year later.

To highlight the challenges small businesses face, as well as the opportunities for resilience and recovery, this report provides a framework drawing on extensive research and original interviews with small business owners and employees that clarifies the nature of weather risks, the sources of disruptions, and the safeguards to mitigate damages.

Narratives of Disruption and Recovery Before, During, and After Severe Weather Hazards

Informed by the real experiences of the small business owners and employees we interviewed, these short, speculative narratives illustrate the types of journeys small business owners follow when preparing for and recovering from a weather hazard.

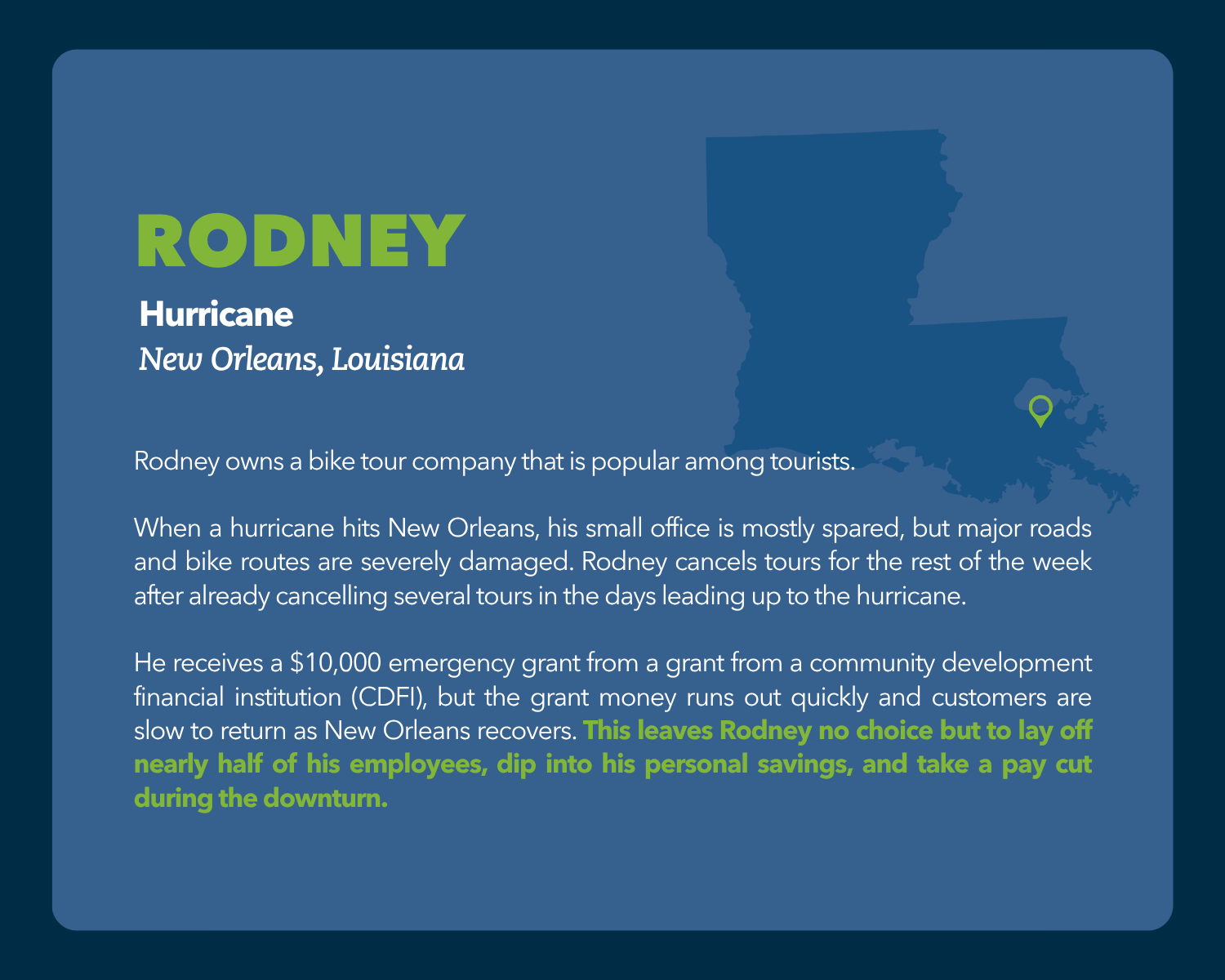

Rodney owns a bike tour company that is popular among tourists.

When a hurricane hits New Orleans, his small office is mostly spared, but major roads and bike routes are severely damaged. Rodney cancels tours for the rest of the week after already cancelling several tours in the days leading up to the hurricane.

He receives a $10,000 emergency grant from a community development financial institution (CDFI), but the grant money runs out quickly and customers are slow to return as New Orleans recovers. This leaves Rodney no choice but to lay off nearly half of his employees, dip into his personal savings, and take a pay cut during the downturn.

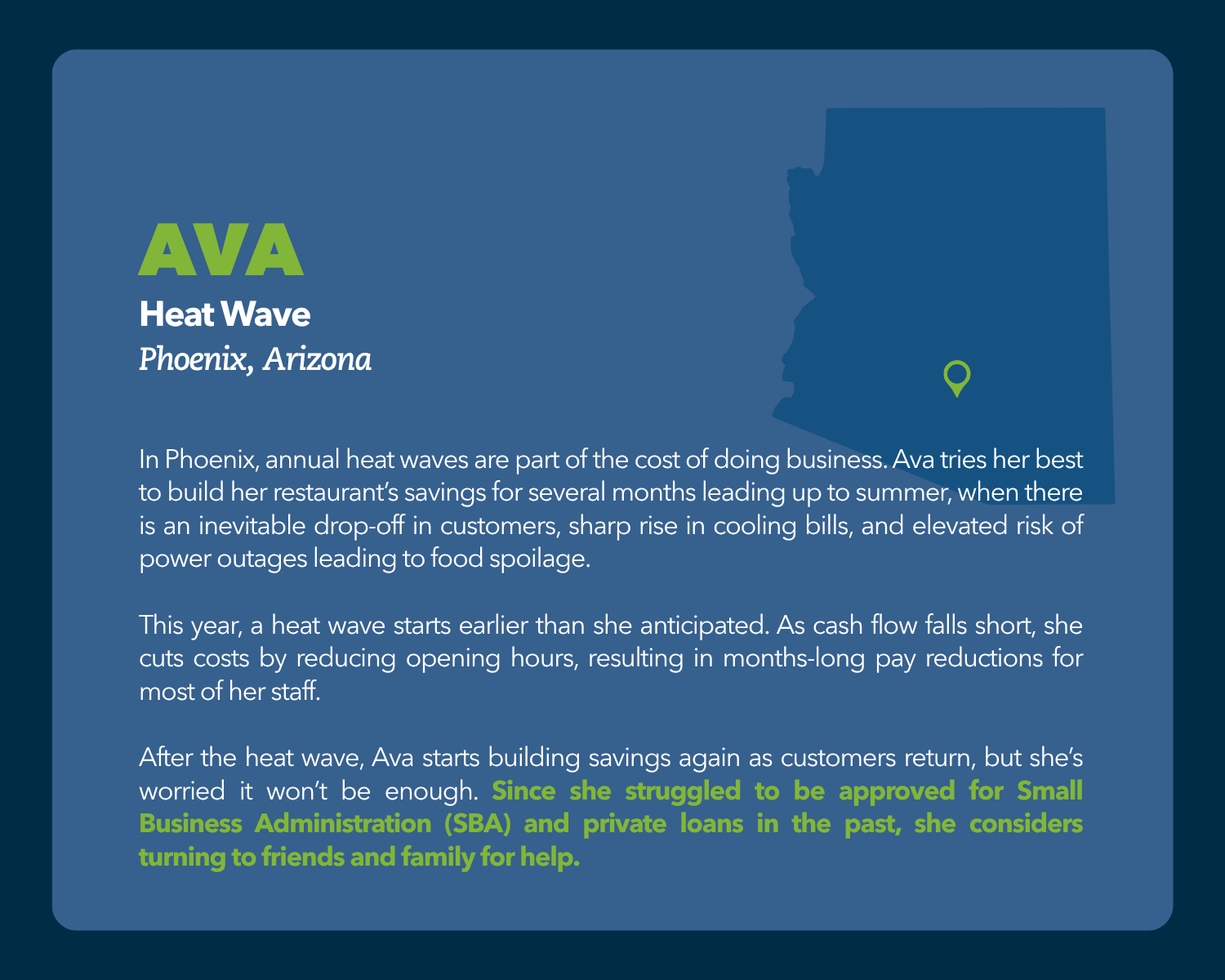

In Phoenix, annual heat waves are part of the cost of doing business. Ava tries her best to build her restaurant’s savings for several months leading up to summer, when there is an inevitable drop-off in customers, sharp rise in cooling bills, and elevated risk of power outages leading to food spoilage.

This year, the heat wave starts earlier than she anticipated. As cash flow falls short, she cuts costs by reducing opening hours, resulting in months-long pay reductions for most of her staff.

After the heat wave, Ava starts building savings again as customers return, but she’s worried it won’t be enough. Since she struggled to be approved for Small Business Administration (SBA) and private loans in the past, she considers turning to friends and family for help.

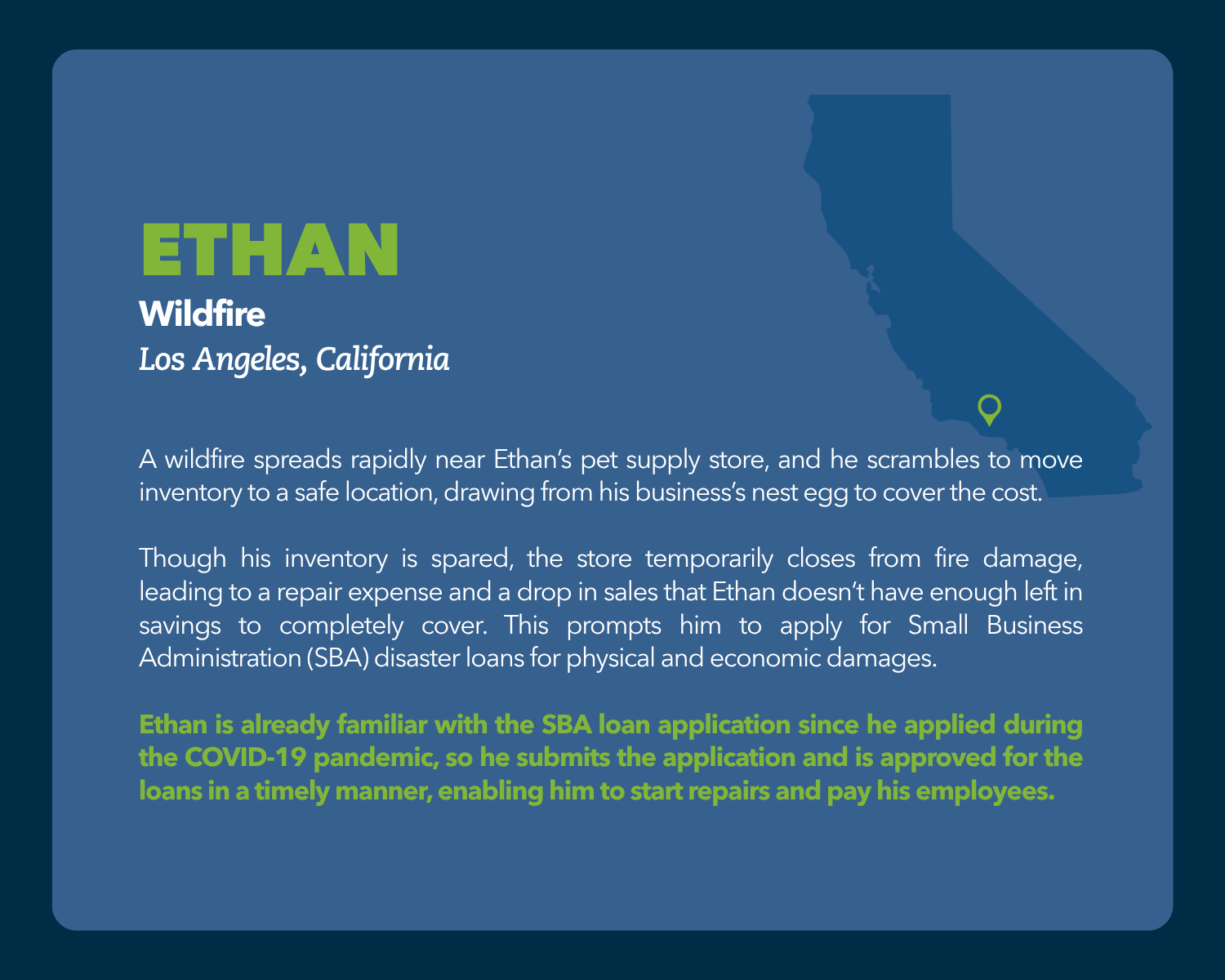

A wildfire spreads rapidly near Ethan’s pet supply store, and he scrambles to move inventory to a safe location, drawing from his business’s nest egg to cover the cost.

Though his inventory is spared, the store temporarily closes from fire damage, leading to a repair expense and a drop in sales that Ethan doesn’t have enough left in savings to completely cover. This prompts him to apply for Small Business Administration (SBA) disaster loans for physical and economic damages.

Ethan is already familiar with the SBA loan application since he applied during the COVID-19 pandemic, so he submits the application and is approved for the loans in a timely manner, enabling him to start repairs and pay his employees.

To learn more about how small business owners are navigating severe weather hazards and how leaders in business support services, finance, government, disaster response, and philanthropy can better support their resilience and recovery, read Surviving the Storms: How Severe Weather Hazards Challenge the Financial Security of Small Businesses.

These personas are informed by the conversations we had with real owners and employees, as well as our background research on the experiences of owners and employees impacted by severe weather hazards. They are illustrative and do not represent any specific individual.

This report was supported by PayPal.

Related

A Gathering Storm: Why The Growth in Climate Hazards Matters for Household Financial Security